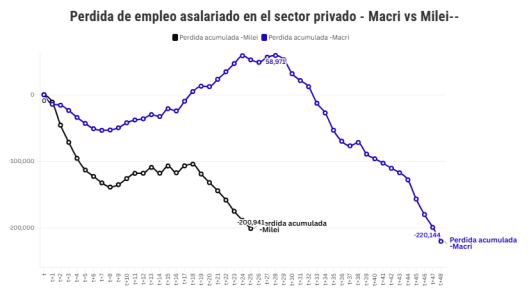

That chart really puts things in perspective. It looks like Macri had a great start. Milei's look terrible. What is honestly going to turn things around?

It's a good example of Macri's gradualism versus Milei's shock therapy. Macri had big plans but he chickened out. It's really politically tough to do what Milei is doing. It's NOT easy to fix a country like Argentina. I've mentioned it many times if you fix one thing two more things break.

While Macri's initial curve looks like a great start if you take a deeper dive of those two lines it reveals why the current situation, though severe, is playing out the way it is and what the necessary triggers are for a reversal.

Macri chose a gradual adjustment path. Because his administration successfully settled with holdout creditors early on, Argentina regained access to international credit. This influx of borrowed dollars allowed the government to avoid slashing public spending immediately, which fueled a temporary economic bounce and job creation (peaking around month 27).

But, when international markets cut off that credit in 2018, the underlying fiscal deficit remained, leading to a massive currency crisis and the catastrophic job losses seen in the second half of his term.

Milei inherited a vastly different landscape. Depleted central bank reserves, NO access to international credit markets, and almost certain hyperinflation. Without the ability to borrow, the administration deployed immediate "shock therapy." He had to aggressively devalued the peso, slashed public spending, and essentially halted public works. This was a deliberate, brutal recession meant to crush inflation and balance the fiscal budget instantly. The resulting drop in consumption and construction is exactly what drove that sharp black line down to -200,000 lost jobs.

It's a great question to ask what will turn it around?

For the trend to reverse and the private sector to start hiring again, several specific macroeconomic dominoes need to fall:

1) Totally Lifting CEPO: They have relaxed some but there are still capital controls in place for companies. This is the ultimate bottleneck. Businesses cannot confidently invest, import necessary materials, or repatriate profits with restricted access to foreign currency. For sectors reliant on capital fluidity and foreign buyers like real estate and property development removing the CEPO is the main catalyst needed to normalize market activity.

2) Labor/Employment Reforms: Argentina’s terrible labor laws carry massive litigation risks and high severance costs, making businesses incredibly hesitant to hire new formal employees, even during a recovery. Broader implementation of labor reforms (like those introduced in the

Ley de Bases) to reduce these liabilities is essential for companies to convert temporary or informal labor into salaried jobs.

3) Kick starting local credit and borrowing: As inflation continues to drop and stabilize, interest rates will follow. The return of viable, long-term credit is crucial. For consumers, this means the return of mortgages, which directly stimulates the housing market and construction. For businesses, including local manufacturing and textile operations, it means access to capital for equipment and expansion.

4) Foreign Direct Investments : The government is heavily banking on the

Régimen de Incentivo para Grandes Inversiones (RIGI) to bring in massive foreign direct investment. While primarily targeted at mining, energy, and technology, the influx of US dollars and infrastructure development from these mega-projects is expected to eventually trickle down to secondary industries and services, creating a bedrock of new employment. However, keep in mind that there is no guarantee that these companies will really invest even if they announce they will. This takes a while to come in and many will probably wait on the sidelines to see how Milei does the remaining 2 years. He has already been involved in many scandals out of stupidity and greed.

Milei's bet is that by fixing the macro-level distortions first (achieving a fiscal surplus and killing inflation), the subsequent recovery will be grounded in genuine private investment rather than debt-fueled public spending. It remains to be seen if it will happen. Personally I believe he tried too much too soon. And they haven't slowed down raising utility and transportation. But his rational is that you have to do it quick and up front while people have some patience but many are running out of steam.